I was born tired and I’ve been having a relapse ever since. So a person could rightfully say I’ve been retired since birth.

Retirement is a state of life that many dream about. Some do not plan for it. Some enter it and find out it is not the Promised Land but a place of strife, unhappiness and possibly financial hardship. The two primary categories I’m addressing today are the financial and lifestyles dimensions of retirement. They overlap and the attention to one will have an impact on the other.

FINANCIAL: It has also been said that free information is as good as the price paid for it. And while this information, along with a five dollar bill, will get you a designer coffee at Starbucks. Hopefully there will be some gems that might be of value.

I have a Bachelors and Master’s degree majoring in accounting and minoring in economics, was a Chief Financial Officer for a number of years and also run my own financial consulting business. In addition I am an avid reader of “The Wall Street Journal and “The Financial Times”.

Let’s start with some basic facts agreed to by most economists.

In 1975 88% of workers with plans covered by their workplace had defined benefit plans, today that number is 35%. More private sector employers switched to 401(k) plans during that time frame with varying degrees of matching which resulted in employees becoming more responsible for their retirement.

A 2010 survey by the Federal Reserve found that the median amount saved through 401(k) s by those households approaching retirement was $100,000. Considering that a person would need to live on that for approximately 20 years one could expect to receive around $417 per month. Couple that fantastic amount with $1,260 (what the average person receives monthly from social security) and you can see why some folks continue to work well after retirement age.

They cannot afford to retire.

You don’t want to be here!

Another consideration is health insurance. In 1988 66% of retirees were covered by an employer’s plan while in 2013 that number has dropped to 23%. Medicare does not cover all medical expenses and therefore obtaining a supplemental policy is a necessity. Medicare Part B is deducted from a person’s monthly retirement check and in 2015 that amount is $104.90 per month. (Hope you’re following the math.)

The number of Americans working beyond the age of 65 has increased. The reasons are the recession, economic necessity from lack of financial planning, or just due to the fact that folks are living longer and they don’t want to outlive their savings. Also many people, myself included, loved what they did and elected to hang on to that part of their life.

Those are the facts. But what is the plan? Outside of searching for a wealthy spouse who is in bad health and has one foot in the grave and another on a banana peel there are a few more realistic options.

Slipping on in!

WHAT TO DO:

First participate in your employer’s 401(k) if they have one. Otherwise begin investing on your own. If your employer has a 401(k) that matches and you are not participating then you are giving up free money!

As regards to investing, there is a simple rule. No one one beats the market year after year. Invest and leave your money alone. Don’t read the stock market reports every day. And if someone is telling you how their company significantly outperforms the market every year, run! Remember, if it seems too good to be true it probably is.

Listen to your wife. Women are far smarter investors than men as has been proven time and again.

Secondly, take a thorough look at your current financial situation. This could be very scary for some but it is better to be scared into action then to be lulled to inaction.

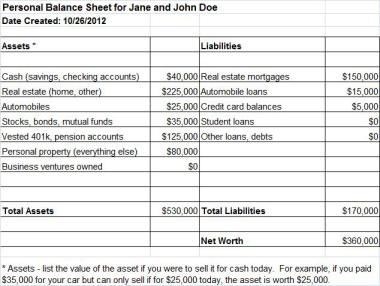

Draw up a balance sheet listing your assets on one side and your liabilities on the other. The difference between the two is your net worth as shown in the example below.

A typical household balance sheet

If your assets are less than your liabilities, you are in a heap of hurt. Also look at your income and compare that to your expenses, or how you spend your money. This may be a real eye opener. Suddenly you may see that cup of coffee or eating lunch out every day adds up to a significant amount.

Wow! That’s what I spend!!

Third, invest in help from books that deal with finance. Some authors I recommend are Dave Ramsey or Suze Orman. Don’t read from authors who are only trying to get you to buy their books or invest in their courses. Or worse yet, promise you great wealth if you do what they suggest. Most of us aren’t going to get there.

Some churches even offer courses on debt management using programs like Financial Peace University which was developed by Dave Ramsey. However, this is not free. Better yet, listen Dave Ramsey’s call in radio show and in a week’s time you’ll learn a lot from other people’s experiences.

A journey starts with one step. Even a procrastinator makes a decision quickly, even if it’s only to procrastinate!

LIFESTYLES: This is basically the quality of life issue that can make or break a person or relationship.

I have heard spouses say, “Good lord, when he retires I’ll have to put up with him all the time” or “living with her day in and day out is worse than being at work”. Other comments I have heard are, “I don’t know what to do, I don’t have any hobbies, etc”.

The retirement years can be dangerous for a relationship due to some significant stress factors. First there is the adjustment to not working. After 40 years of employment the end of that can be similar to a death.

Second, there is reduced income which can impact a couple’s lifestyle.

Third, there is the adjustment to the relationship. From being newlyweds to raising children and becoming grandparents, you now are together again without anyone else around. You signed up for better or worse. Let’s hope it’s for the better.

Consider this fact that the number of divorces of those 50 and older doubled from 1990 (4.67%) to 2010 (9.74%). Today there is a term called “gray divorce” (though it may not have 50 shades). This refers to people in that age group. Looking for a real joy stealer? Become a statistic where the two of you divide up the assets (after the lawyer’s fee), and then maintain two households.

Building a lasting relationship, one that will survive retirement, starts with a four letter word, “WORK”. Around our house are two very opinionated, strong willed independent people who have managed to make a go of it in spite of the fact that some folks at our wedding placed bets on how long the marriage would last. The first thing is to have an unconditional love towards your spouse and keep them, not your children or grandchildren and not your hobbies, a priority.

Next, share things in life. Hopefully you had similar interests when you married including faith. If you didn’t before, you can certainly find some now. Again, it’s called “work”.

Doing things together

Enjoy each other’s company. Whether it is travel, reading books, skiing, kayaking, shopping or just having a weekly date night.

As we age, we begin to have health issues. Parts wear down and need to be replaced. Look at the bright side. If you don’t set off the scanners at the airports or stick to magnets, then you are doing okay. Disease can impact anyone at any time, however there are things we can do to reduce some of the factors.

We can maintain healthy lifestyles so those retirement years can be enjoyed. Contributing to our own health is probably the most important area where couples can make the biggest difference. Stop smoking. Drink in moderation (moderation means an occasional beer or an occasional glass of wine). Lose weight. Eat a sensible diet. Find time to exercise. Start out by walking and as you get more in shape add to the regiment with strength building. Consider a gym membership if you need that extra support. Some are quite inexpensive.

The third component to finding joy in retirement is to have a plan regarding what this newly “found” time means to you. Sitting in the chair and watching television is not consistent with an active healthy lifestyle. Find activities that challenge your mind, body or spirit. Volunteer with a local agency, work with Habitat for Humanity, or find some other outlet that will put good use to the skills you have acquired over a lifetime.

Romantic spots

This can be the most rewarding time in a person’s life if they plan for it.

On the beach in Australia

(I’ve asked my wife to write a guest post for me to give the female perspective to all this. After all, retirement is about the two of you, not the one of you.)

Good blog Doug. A lot of it is why I am still working. Thanks for the thoughts.